Forget the “Fed Follies”

Here's where the real money is buried ...

To cut or not to cut …

When it comes to the U.S. Federal Reserve’s interest-rate policies (and with apologies to William Shakespeare), that isn’t the real question we need answered.

At least it isn’t the question that’s paramount to Wealth Builders like you and me.

But after policymakers failed to act today, exactly when the Fed will start cutting rates – and by how much … and over what time frame – is the headline du jour.

So let’s take a quick look at this story – such as it is. Then let’s look at what really matters for you – and your money.

Standing Pat

The Fed didn’t act today – meaning interest rates remain at their current 5.25%/5.5% levels, a 23-year high.

In its statement, America’s central bank conceded that “in recent months, there has been a lack of further progress toward the [policymaking Federal Open Market Committee’s] 2% target” for inflation.

As you folks know, I like to keep things simple here – and part of that means I wring out the jargon/gobbledygook/brokerspeak.

I actually preferred some of the characterizations of some of my financial-writing brethren who said the Fed’s assault on inflation “is stalling.”

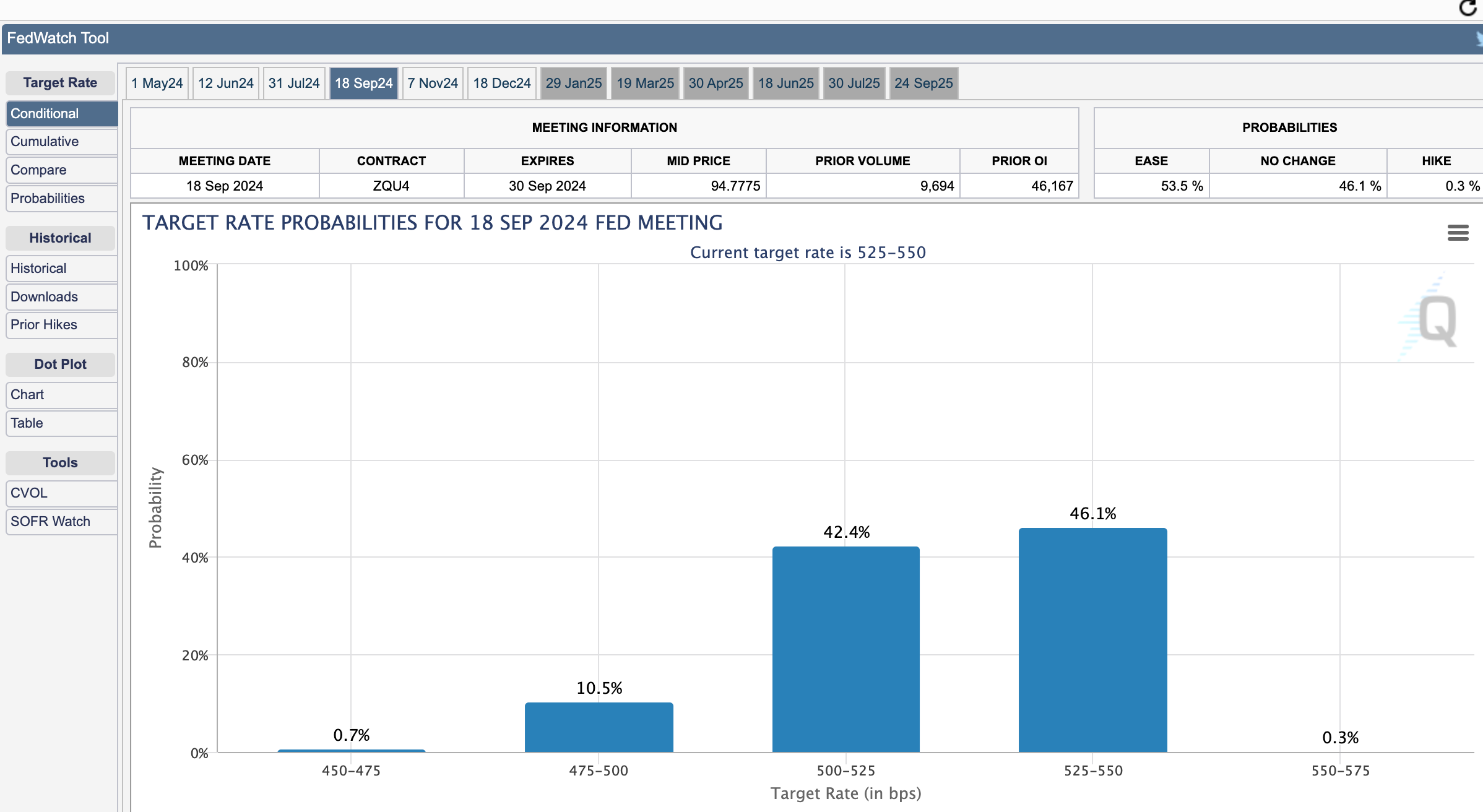

And according to the CME FedWatch Tool, you shouldn’t expect big cuts.

Not big ones. And not soon.

As I write this, there’s a 90% chance the Fed takes a pass (and holds the line) at its meeting in June and a 74% chance in July.

As far out as September, FedWatch is handicapping a 53.5% chance of a rate reduction. Even then there’s still a 46.1% chance Team Powell keeps rates unchanged.

Look, I’m not minimizing this from a near-term stock market or U.S. economy point of view.

The Fed’s “higher-for-longer” balancing act has been just that: On one side we’ve got an inflation problem that refuses to go away and a pickup in hiring; on the other, we’ve got a slowing economy, stock valuations predicated on an optimal backdrop and worries (by some) that a recessionary threat peeks at us from the shadows.

"I think we have to recalibrate" our expectations vis a vis Fed rate cuts, Austan D. Goolsbee, president and CEO of the Federal Reserve Bank of Chicago said recently. "It doesn't look like it's going to be as rapid as it looked for the previous six or seven months."

What Really Matters

I promised I’d show you what really matters. And I keep my promises.

So here it is.

This game of “Rate-Cut Roulette” just doesn’t matter.

Not really. Not in the long run. Not where real wealth is built.

And I’ll prove it.

Right here. And right now.

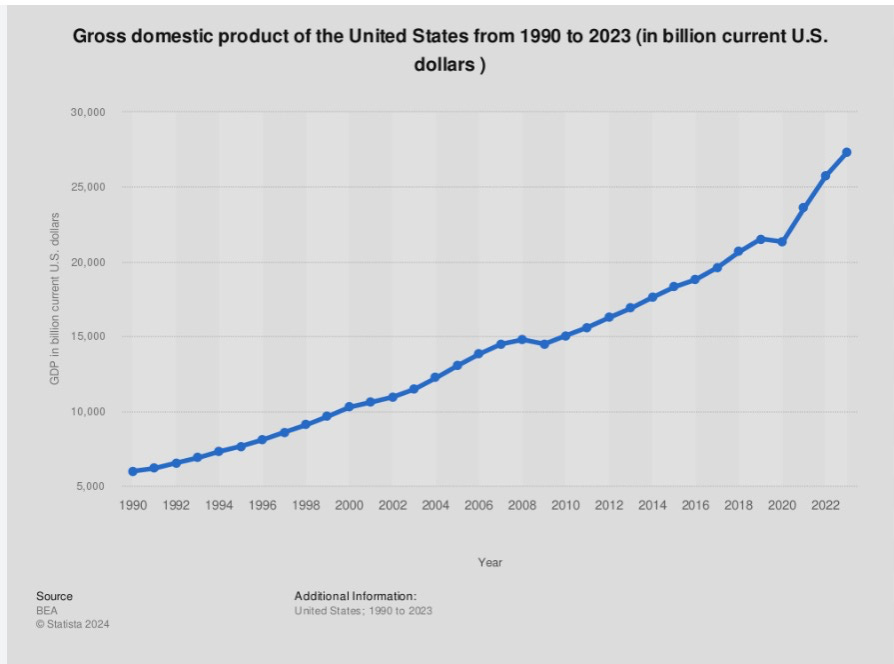

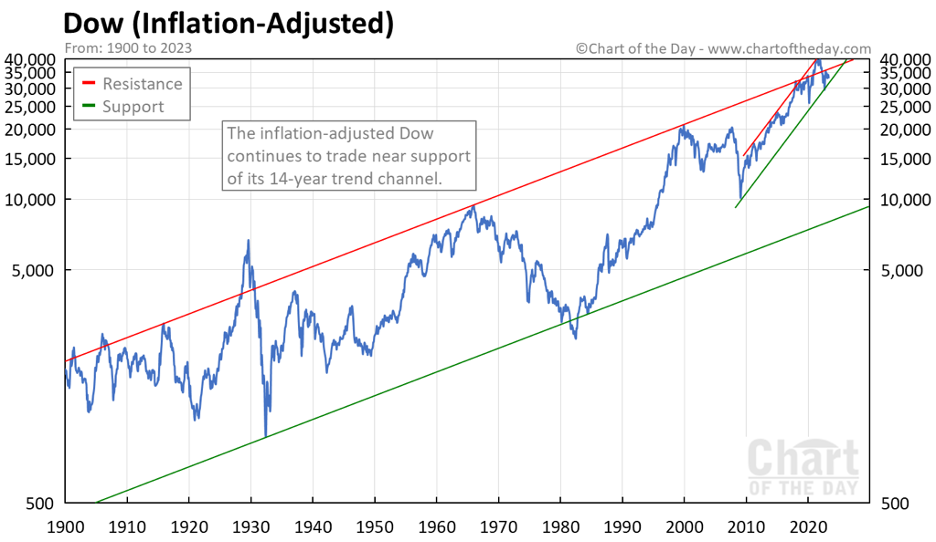

In 1900, the U.S. economy was worth $590 billion. And the Dow Jones Industrial Average – not quite four years old at the time – opened that New Century at 66.08.

Since that time, we’ve been through World War I and World War II, the Korea and Vietnam wars, two Gulf Wars, the beginning and end of the first Cold War, and the start of the New Cold War, 9/11, countless presidential elections, the Panic of 1907, the Great Depression, the Great Financial Crisis and the Great Recession, the Crash of ’29, the Crash of ’87, the civil rights protests of the 1960s, Watergate, the Savings and Loan Crisis, the Dot-Com Bubble, the COVID-19 Pandemic, and those are just the highlights.

Today, the U.S. economy has grown to $28.78 trillion – nearly 49 times bigger.

And the Dow has zoomed to 37,815 – 572 times higher.

So why am I telling you this?

Simple.

Both the U.S. economy and U.S. stocks tend to rise over time. And longer stretches put the odds – and profits – on your side.

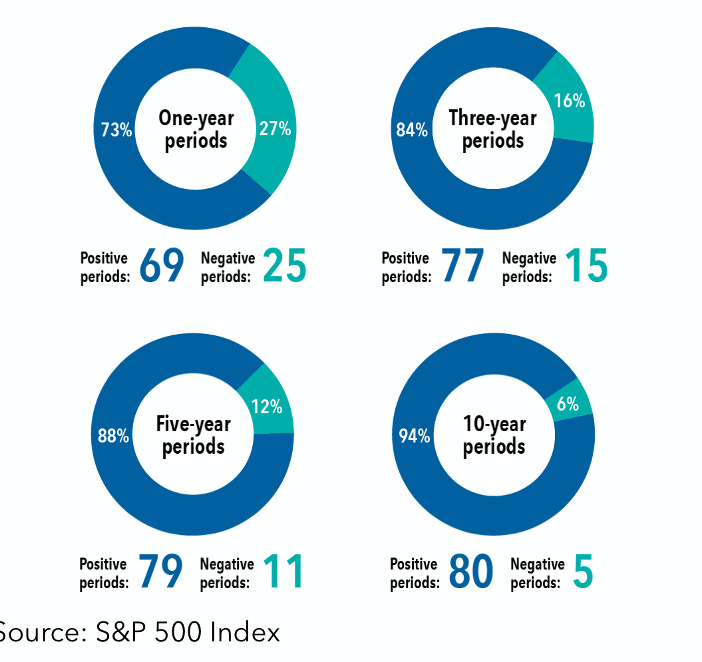

For Wealth Builders like us, it’s the long run that matters. Indeed, if you look at the stretch between 1928 and 2022 – and slice that into 10-year increments – 94% have been positive.

As that chart from Standard & Poor’s and American Century shows us, even shorter holding periods put the odds in your favor.

So it’s not necessarily “timing” your investments to important “events” like, say, a Fed meeting that revs up your wins. It’s “time in the market” that sets you up as a Wealth Builder.

And with good reason.

The longer you go, the greater the odds you’ll navigate “events” like some of the ones I listed above. The better the chance that you can “smooth out” the near-term whipsawing that tends to accompany them. And the greater the chance you’ll have at smoothing out any of the mistakes that all of us occasionally make.

I’m not necessarily advocating a “buy-and-hold-forever” strategy.”

In his book, “Same As Ever: A Guide to What Never Changes,” (Disclosure: As an Amazon Affiliate, we may earn commissions from qualifying purchases on Amazon) author Morgan Housel tells us that a 10-year holding period is the ideal span – for generally the same reasons I’ve outlined here.

Indeed, that longer view is part of the the strategy I advocate here at Stock Picker’s Corner (SPC) – a strategy underscored by the reality that:

We’re Wealth Builders, Not Wealth Killers: We invest – we don’t trade. We go for the big gainers.

We Find the Best Storylines – and Then Find the Best Stocks: Wealth Builders know that powerful narratives (back to this in a second) lead to those powerful gains.

We Accumulate Our Way to Wealth: We buy those “Best Stocks” on pullbacks.

And We Hold For the Long Run: Save for some special-situation plays, we’re not looking to pick off profits here and there … we’re looking to stack wealth.

Super Storylines Lead to Super Wealth

I like to make things as simple for you as possible. That simplicity is a superpower, of sorts, because it makes you an efficient and effective Wealth Builder.

So when stocks go up, we make money.

When stocks go down, we look at our long-term storylines and look at what we want to be buying.

Just what are those storylines I keep telling you about?

Here are five I’ve already detailed here at SPC:

The AI Era, which is more than just chipmakers. One company mentioned: Blackstone Inc. BX 0.00%↑.

Essential Income, which demands a “bottom-line,” cash-flow mindset for high-yield wealth plays. One true “passive-income” play mentioned: Annaly Capital Management Inc. NLY 0.00%↑.

Special Situations, which include spinoffs and opportunities in silver and copper.

The New Cold War, which intersects with AI and Special Situations, is helping drive deglobalization, and which will drive hefty opportunities in drones, cybersecurity, defensive weaponry, and more.

The New Biotech, which will be defined by the Next Blockbusters, personalized medicine, AI and data, and consolidation. Among the beneficiaries we’ve talked about here are the new class of GLP-1 weight-loss drugs being marketed by companies like Novo Nordisk NVO 0.00%↑ and Eli Lilly & Co. LLY 0.00%↑, and the leading “Pet Biotech” Zoetis Inc. ZTS 0.00%↑.

I’m looking at several other powerful storylines, too.

I’ll keep bringing them your way … so be sure to keep visiting.

See you back here next time;