Financial Literacy: How I Started My Son Toward His First Million Dollars

My Wealth Builder “Best Buddy” Makes ME a Rich Man

When my son Joey was little, he proclaimed that he and I were “Best Buddies” – because Best Buddies were even closer than best friends.

I treasure that moment. Just as I treasure every single time one of us uses that term of affection anew.

I’m a lucky man – I’d even label myself as “rich” – because I’ve got a son I can be super proud of … and because that son still likes to spend time with me.

Rock concerts. Trips to other cities to see and do cool things. Major League and Minor League ball games. NASCAR races at Bristol and Dover. Car shows (in the last few weeks alone, we’ve been to four). I coached him through rec ball (he’s got one heck of a swing). I never miss his school concerts. Or his cross-country or track meets. I bought him his first electric guitar (it was during COVID, and it was quite the effort to “bird dog” just the right one). And I built him his first electric bass.

I also taught him how to drive – starting when he was 12, in parking lots and on private roads; when he finally got around to taking his driving test, my son already had hundreds of hours behind the wheel.

And now that he’s finished his junior year, Joey, my wife and I are starting with the college visits. (We have a trip this week to visit the University of Delaware.)

And just as I got an early start with Joey’s driving lessons, I made sure my son got an early start understanding money – or as it’s known in the jargon of investing: “Financial literacy.”

SMART MONEY SON

Financial literacy is a personal hot button for me.

And I put my money where my … son … is.

A few years back, when Joey was 12, I put a few thousand dollars in a custodial account, sat him down, and said: “Buddy, we’re going to get you started investing, and we’re going to do it together.”

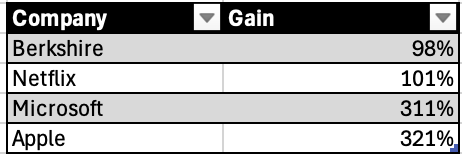

I made sure to personalize it a bit, by talking about things Joey liked and used and was interested in. He loved xBox and Minecraft, so we bought some Microsoft Corp. MSFT 0.00%↑. He loved his iPad and iPhone and iTunes account, so we bought Apple Inc. AAPL 0.00%↑. He was a devotee of Netflix Inc. NFLX 0.00%↑, so we bought that. His favorite food was mac & cheese, so we bought some Berkshire Hathaway (BRK. A, BRK.B), which owned Kraft Heinz.

I grant you: It was only a few shares of each stock … but making money (which, as I’ll show you shortly, he certainly has) was only part of the goal: I also wanted to “sensitize” him to money, the economy, investing and the financial markets.

Our financial foray worked great. As mentioned earlier, Joey just finished his junior year at a high school near Baltimore. He signed up for a business class that was offered. He has a part-time job. A bank account. A small credit card. And a Ford Fusion that I “gave” him that he takes good care of, takes to the car wash to vacuum and clean – and keeps filled with gas.

He’s fascinated by the Stock Picker’s Corner (SPC) publication here on Substack. (The first thing he does when he gets home from work or when I pull in is to ask: “How did your business do today?” He even understands how to punch up our analytics on my MacBook. All this interest absolutely thrills me.)

As I showed you with our report on the State of the Union message, he has a working understanding of inflation. He’ll often comment about headlines or announcements made by the companies he invested in.

And, as I said I’d show you, he got his own “head start” – on his personal fortune.

WEALTH BUILDER/WEALTH KILLER

Joey is by no means an expert … but that’s okay: We’ve given our son a “situational awareness” about financial issues … meaning he’ll pay attention as he gets older, goes off to college and moves out on his own.

Every parent should give their kids that kind of financial foundation. Except that lots of parents don’t possess that themselves.

One interesting aside. When I helped Joey with his initial stock-market foray, I wrote about it in my previous newsletter, Private Briefing.

I was surprised (actually, I was stunned) by the number of co-workers … colleagues of mine at a financial publisher in their 20s, 30s and 40s … who said they’d read my column – and wondered if they should start investing for themselves this way.

(It was downright alarming to me to see folks in their 30s and 40s who’d never owned a stock, didn’t have investments, weren’t investing in their 401(k)s and clearly didn’t understand “money basics.” The fact that they owed their livelihoods to a company whose prime directive was investing elevated my “alarm” to “terror” when I started thinking about America’s Wealth Killer future.)

But starting at any age is better than doing nothing at all. And the younger you start, the more likely you’ll be a Wealth Builder and not a Wealth Killer – and the bigger the back-end bang you’ll reap.

And though I’ve only been part of the Substack ecosphere for less than six months, I can already tell from the subscribers who’ve joined us and the fellow writers who’ve reached out that we’re part of a community whose members are smart and open to new ideas.

For me, that’s yet another reminder that Substack is the place to be.

For you … you’ve put yourself on a path to being a Wealth Builder.

Wealth Builders:

1. Know who they are – Wealth Builders don’t invest in companies and assets or use “tools” that they don’t understand.

2. Know they need an “accumulation strategy” – Wealth Builders understand how to find the “right” stocks – and use that knowledge to consistently build meaningful stakes.

3. Know they won’t get rich overnight – Wealth Builders make time an ally, and leave options and margin trading to everyone else.

4. Know when to cut their losses – Wealth Builders understand that mistakes are inevitable. They know everyone makes bad investments. Instead of beating themselves up, they use it as a teaching moment. And they move on to the next opportunity.

5. Know their exit strategy – Wealth Builders have a pre-determined plan of when to cash out and walk away from an investment.

6. Know that the best storylines lead to the best stocks –Wealth Builders don’t chase short-term trends or market fads. And they don’t succumb to “Malarkey-esque,” Wealth-Killing gambits.

I laud you for being a Wealth Builder.

Oh … and about my point about getting a multi-year head start with Joey on investing and driving? I’m getting a head start in another place, too: I’m getting a multi-year running start on missing him after he leaves for college (lol). Fortunately, there’s a remedy: Make more memories before he leaves.

(Yeah, “Old Bill” is already realizing how wrenching that “leaving for college moment” is going to be.)

See you next time.

This is so awesome to see. Like you mentioned it is less about the money he's gained and more about the habit he has built. Awesome job. I hope this post inspires more parents to do the same with their kids!

This column comes up in conversation AT LEAST once a week ...

https://substack.com/@stockpickerscorner/note/c-72657587?utm_source=notes-share-action&r=3ftiph