The Substack Chat: Three of Us Share Notes on PayPal

And what's next for PayPal ...

Over the past few weeks, I’ve had the chance to share thoughts about PayPal Holdings Inc. PYPL 0.00%↑ with several other investing-focused Substackers.

The first exchange involved this Watch List of “unloved” software/tech stocks (it’s a pretty intriguing list worth checking out) created by Value Don’t Lie.

The second exchange related to this PayPal-specific research report was created by Schwar Capital.

After an early-August selloff that chopped PayPal down — back into the high $50s — the stock gas surged of late, powering its way back into the low $70s.

But it’s the long run that counts.

The upshot from all of this: Although I’d like to do a bit more digging, I told both these researchers that it looks to me like PayPal has the potential to be a company for Wealth Builders.

“So, I tend to super-simplify things,” I told them. “But let’s say we apply the old Peter Lynchian ‘invest in what you know’ (ie: ‘invest what you use’) precept as a base-level screener. I mean, as a consumer, I use the heck out of it. For eBay Inc. EBAY 0.00%↑. For buying stuff for my old Hot Rod (which needs a new battery, now that I think of it). PayPal’s Fastlane checkout innovation seems to have legs (I saw it has a new deal with Adyen NV (ADYEY). And it looks like earnings are projected to grow in the high teens for the next few years … I like longer holding periods … as we’re Wealth Builders, not “traders.”

As I underscored in both discussions: “Not a recommendation, mind you. Just a response to [an] intriguing … query.”

So that’s my “executive summary.”

Let me add a bit more here — as I said, just for you folks.

Point No. 1: Earnings Are Projected to Accelerate

Look, we all know that profit forecasts are exactly that — forecasts. And the further out you go, the less reliable they are — in terms of specifics.

But they at least give us something to work with — and can provide us with a feel for direction (up, down or flat), magnitude (a little or a lot) and a point of comparison with peer companies, shares of other companies — and the market in general.

After an average annual profit growth of 11.69% over the last five years, PayPal’s profits are projected to grow at an average annual clip of 19.45% over the next five. That’s better than the Standard & Poor’s 500 average of 10.42% — nearly double, in fact.

At that pace, PayPal’s profits would double in 3.7 years. All else being equal (or ceteris paribus as my business school economics prof liked to say … I love that term), share prices tend to follow profits — if not precisely, then at least in terms of direction and magnitude.

And that leads us to the next point …

Point No. 2: PayPal’s Share Price Is Projected to Zoom

Once again, Wall Street estimates are notoriously unreliable (I’ll share some stories from my days as a business reporter covering public companies). But, again, taken as data points that can be used in conjunction with other numbers, and the “storylines” we like to see, these projections are perfectly fine to consider.

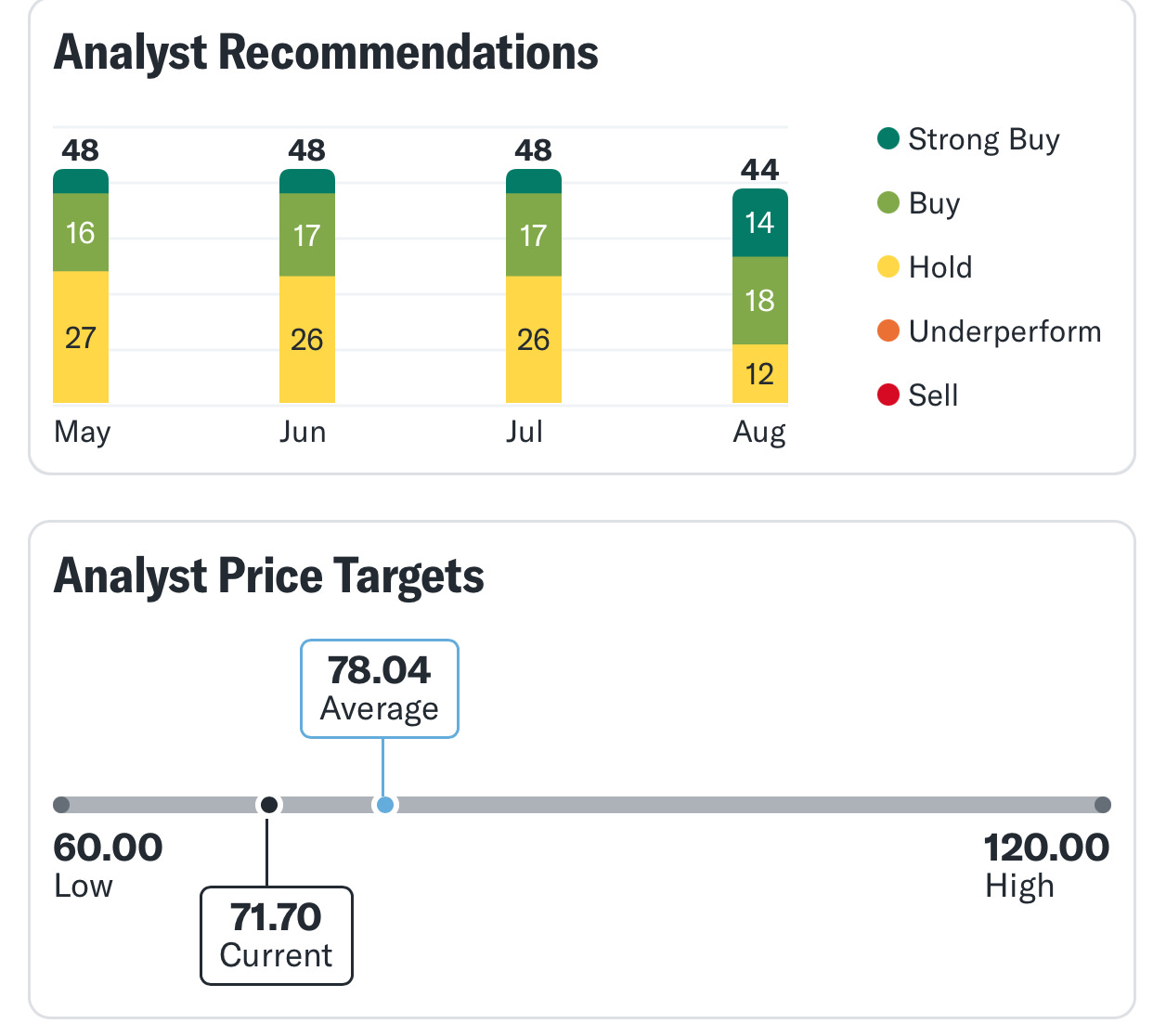

Analysts have grown more bullish — with more “Buy” and “Strong Buy” ratings, of late. And the number of “Hold” ratings has fallen by more than half.

PayPal was recently trading at about $72. The current consensus target is about $78 — or about 8.3% higher than that current price. Those “targets” are typically for 12 months to 18 months from the time they’re delivered. And the current “high” estimate — meaning the top target price posted by a sell-side analyst — is $120. That’s 67% above PayPal’s current stock price.

Again, these are all analyst projections … so they’re more for context than “greed triggers” for us.

For me, it’s the “storylines” that are worth delving into.

And the latest story is the one I chatted about with the two other Substackers …

Point No. 3: PayPal’s “Story” Is Getting More Interesting

The San Jose-based PayPal is one of the world’s leading fintech firms, specializing in payment processing. It was part of eBay at one point and was spun off as a standalone company in 2015. It’s a strong brand — in fact, it is one of those ventures whose name has become “a verb.” Just think about that: How many times have you heard someone say “I’ll PayPal you.” Maybe you’ve said it yourself.

It’s easy to use. And it’s always been an innovator. And it’s massive: We’re talking about a global payment network — connecting about 430 million consumers and more than 35 million merchants. Fees from transactions account for about 91% of its revenue —and most of that came from PayPal-branded payments. It also owns Venmo — the peer-to-peer payment app that’s really popular with the younger set.

One of the newest developments involves Fastlane, an app PayPal licenses to merchants. Once a customer has a transaction with that participating business, their credit cards and payment information can then be prefilled automatically on their next purchase. PayPal says it reduces the time to check out by 32%, and Fastlane has been getting terrific reviews since its launch in January.

Now PayPal has struck a deal with Adyen, a Dutch company with highly regarded payments-platform technologies. Now Adyen can offer Fastlane to its customers in Europe, the Middle East, Africa, North America, the Asia Pacific and Latin America.

The deal is essentially a “seal of approval” for Fastlane — elevating its status in the “fast-guest-checkout” market.

This is a “big step forward in Fastlane establishing itself as a credible, independent leader” — especially because of Adyen’s platinum customer roster, says JPMorgan analyst Tien-Tsin Huang.

Fastlane may not get real traction in the Adyen network before the important 2024 holiday shopping season. But that means the impact will be big in 2025 — meaning you can buy PayPal now and reap the benefits from this deal next year.

Schwar Capital ended its report by stating that PayPal’s “upside is driven by multiple promising catalysts that could transform PayPal’s business under the guidance of a capable new management team [which] is why PayPal is our largest holding.”

Point No. 4: Our Very Best Ideas …

Is this enough to add PayPal to our SPC Premium “Farm Team?”

Or even our SPC Premium “Model Portfolio?”

We need to do more research on PayPal — and we will — before we know for sure.

After all, only our very best ideas are outlined in our super-detailed SPC Premium Dossiers.

And we craft detailed briefings as the underlying storylines for these “Best Idea Companies” develop in our Premium Issues.

This absolutely is a stock we’ll be digging into again.

See you next time …

P.S. I asked Value Don’t Lie for his “take” on my PayPal insights. And I also asked him what other stocks on his Watch List he liked.

He said that PayPal — as well as Dropbox Inc. DBX 0.00%↑ and Yelp Inc. YELP 0.00%↑ “were ‘in use’ personally.”

And he said that “YELP might be top of pile for me from investment standpoint.”

Check out his list (here’s the link again). Take a look and share your thoughts with him in the comments where I did. And tell him Bill from Stock Picker’s Corner sent you.

Thanks for the mention!